What are the classes of depreciation?

What are the classes of depreciation?

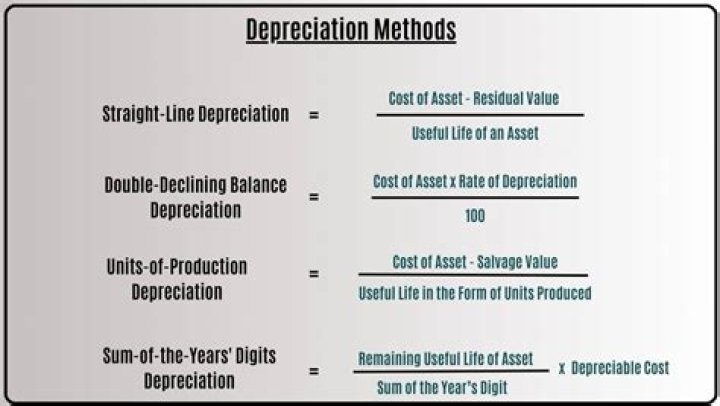

What are the Main Types of Depreciation Methods?

- Straight-line.

- Double declining balance.

- Units of production.

- Sum of years digits.

What is class life for depreciation?

The class life is the IRS’s estimate of the average useful life of assets used in that industry. Once the class life for an industry or business activity is determined, depreciation periods for the assets used in the industry are determined under the following schedule: MACRS depreciation period for industry assets.

What is a depreciation asset class?

The depreciation class contains the information used to calculate the asset depreciation over its useful life. A depreciation class is linked to an asset-type item and the information contained in the class is used to calculate the depreciation for the assets associated with this item.

What are 7 year assets?

7-year property. 7 years. Office furniture and fixtures, agricultural machinery and equipment, any property not designated as being in another class, natural gas gathering lines.

What is 25 year property for depreciation?

25-year property – water treatment facilities. Residential rental property – rental apartments or homes. Nonresidential real property – office buildings or stores.

How do you calculate tax depreciation?

The straight-line method is the simplest and most commonly used way to calculate depreciation under generally accepted accounting principles. Subtract the salvage value from the asset’s purchase price, then divide that figure by the projected useful life of the asset.

What is 7 year property?

7-year property. 7 years. Office furniture and fixtures, agricultural machinery and equipment, any property not designated as being in another class, natural gas gathering lines. 10-year property.

What is 25-year property for depreciation?

What is 15 year property for depreciation?

Businesses can now treat QIP placed in service after December 31, 2017, as 15-year property. It is eligible for bonus depreciation, allowing taxpayers to deduct up to 100% of the cost of assets that are being depreciated over 39 years under the previous law.