What will be the equilibrium condition for long run?

The long-run equilibrium of a perfectly competitive market occurs when marginal revenue equals marginal costs, which is also equal to average total costs.

What is the condition for producer’s equilibrium?

Producer’s equilibrium refers to the state in which a producer earns his maximum profit or minimise its losses. According to MR-MC approach, the producer is at equilibrium,, when the Marginal Revenue (MR) is equal to the Marginal Cost (MC) and Marginal Cost curve must cut the Marginal Revenue curve from below.

What happens to equilibrium price in the long run?

The long-run equilibrium requires that both average total cost is minimized and price equals average total cost (zero economic profit is earned). The long-run equilibrium price equals $60.00. So the firm earns zero economic profit by producing 500 units of output at a price of $60 in the long run.

What do you mean by equilibrium of the industry in long run?

The industry is in long-run equilibrium when a price is reached at which all firms are in equilibrium (producing at the minimum point of their LAC curve and making just normal profits). Under these conditions there is no further entry or exit of firms in the industry, given the technology and factor prices.

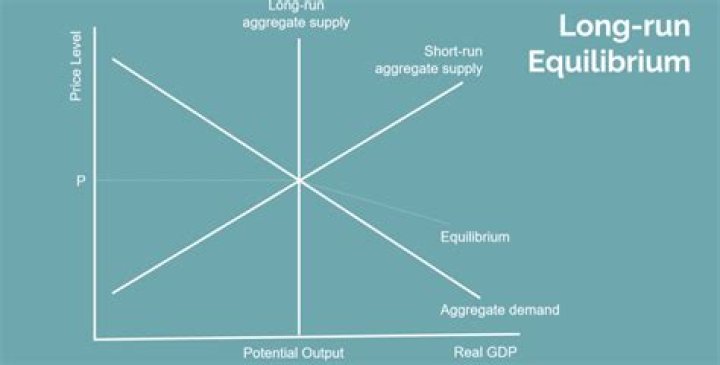

What happens when equilibrium is below long run aggregate supply?

Long-run equilibrium occurs when the current output is also equal to potential output. If the price level decreases below equilibrium, then you have a shortage in GDP. This means that your aggregate demand is greater than your aggregate supply.

What are the conditions for producer equilibrium Class 11?

Producer’s Equilibrium : A producer or firm is said to be in equilibrium when it produces that level of output which gives him maximum profit and he has no incentive to change its existing level of output.

What are the conditions for a firms equilibrium in MC & MR approach?

According to this approach, the firm is said to be in equilibrium if the following conditions are fulfilled: Marginal cost is equal to Marginal Revenue i.e. ( MC = MR ) Marginal cost (MC) Cuts Marginal Revenue (MR) from Below. Marginal cost (MC) Cuts Average Cost (AC) from the Minimum point.

What is the condition for long run equilibrium in monopoly market?

The conditions for Equilibrium in Monopoly are the same as those under perfect competition. The marginal cost (MC) is equal to the marginal revenue (MR) and the MC curve cuts the MR curve from below.

What are the conditions for long run equilibrium of a perfectly competitive market explain with the help of suitable diagram?

The long-run equilibrium point for a perfectly competitive market occurs where the demand curve (price) intersects the marginal cost (MC) curve and the minimum point of the average cost (AC) curve.

What are the conditions for long run equilibrium in monopoly market?

A Firm’s Long-run Equilibrium in Monopoly Therefore, to determine the equilibrium of the firm, we need only two cost curves – the AC and the MC. Further, since the monopolist exits the market if he is operating at a loss, the demand curve must be tangent to the AC curve or lie to the right and intersect it twice.

What is long run and short run in macroeconomics?

In macroeconomics, the short run is generally defined as the time horizon over which the wages and prices of other inputs to production are “sticky,” or inflexible, and the long run is defined as the period of time over which these input prices have time to adjust.