What is valuation allowance for deferred tax?

A deferred tax asset is a tax reduction whose recognition is delayed due to deductible temporary differences and carryforwards. A business should create a valuation allowance for a deferred tax asset if there is a more than 50% probability that the company will not realize some portion of the asset.

What is deferred tax on capital allowances?

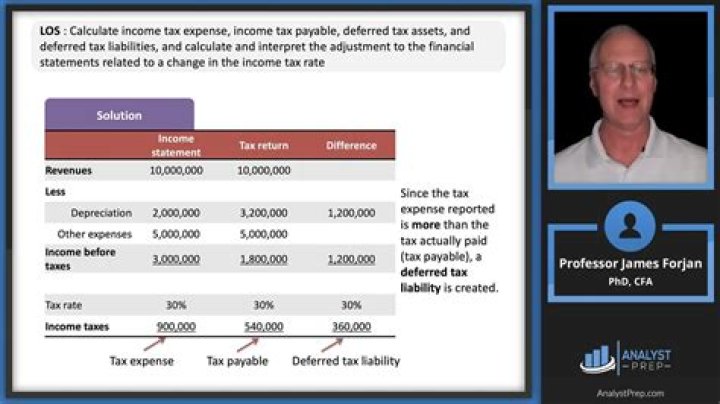

One of the most common deferred tax liabilities arises from the differences between the depreciation charged on a non-current asset compared to the capital allowances given for that asset. In situations where capital allowances exceed the depreciation charged, this will result in a deferred tax liability.

How should a valuation allowance be presented in the balance sheet?

Valuation allowances can be made under the deferred tax asset entry of a balance sheet and shown as an offset in parenthesis. This calls attention to the fact that there’s a valuation allowance and clearly shows what the impact is on the total value of the deferred tax asset.

How are valuation allowances allocated?

A valuation allowance is a reserve that is used to offset the amount of a deferred tax asset. The amount of the allowance is based on that portion of the tax asset for which it is more likely than not that a tax benefit will not be realized by the reporting entity.

How do you calculate deferred tax?

Multiply the average tax rate by the temporary difference to get the deferred tax liability or asset. For instance, at tax rate of 30 percent, a deferred tax liability or benefit for a $2,100 would generate a deferred tax of 30/100 x $2,100 = $630.

What is deferred tax with example?

One straightforward example of a deferred tax asset is the carryover of losses. If a business incurs a loss in a financial year, it usually is entitled to use that loss in order to lower its taxable income in the following years. 3 In that sense, the loss is an asset.

How is deferred tax treated?

If any amount claimed in Income Tax is more than expensed out in Profit & Loss A/c, it will create Deferred Tax Liability. The net difference of DTA / DTL is computed and transferred to Profit & Loss A/c. The Balance of Deferred Tax Liability / Asset is reflected in Balance sheet.

When should a deferred tax asset be reduced by a valuation allowance?

The assets should be reduced to the amount that more likely than not can be recovered—meaning there is a greater than 50% chance that the remaining assets are recoverable.

Where is deferred tax asset on the balance sheet?

Conclusion. Deferred tax assets in the balance sheet line item on the non-current assets, which are recorded whenever the Company pays more tax. The amount under this asset is then utilized to reduce future tax liability.

When can a firm reduce a deferred tax asset by a valuation allowance?

After deferred tax assets have been recognized, firms must reduce deferred tax assets by a valuation allowance if “it is more likely than not (a likelihood of more than 50 percent) that some portion or all of the deferred tax assets will not be realized” (ASC 740-10-30-5).

How is deferred income tax calculated?

Subtract accounts payable and employee compensation funds from the total equity. Research tax rates and all possible tax deductions. Subtract deductions from each asset category. Add together taxable assets, and multiply by an accurate or assumed income tax rate to create an estimate of deferred income tax liabilities.