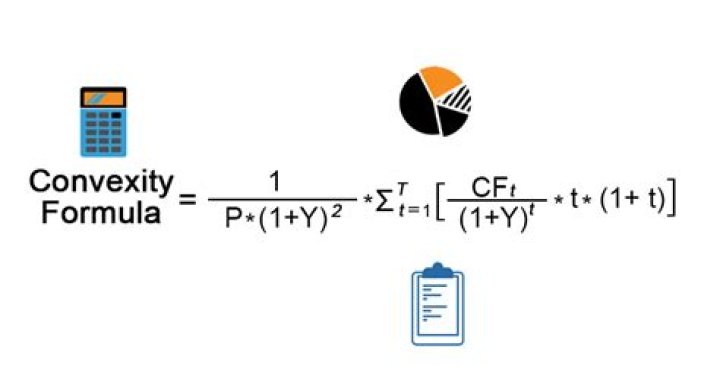

What is the formula for bond convexity?

Calculating Convexity To approximate the change in the bond’s price given a particular change in yield, we add the convexity adjustment to our original duration calculation. Convexity (C) is defined as: C=1P∂2P∂y2. where P is the bond’s price, and y its yield-to-maturity.

How is convexity derived formula?

With the above intuitive understanding, let us calculate convexity. Convexity can be defined as ΔMD/ΔY – ie the change in MD divided by the change in yield. Now MD itself = ΔP/ΔY.

How do you calculate convexity of a bond portfolio?

So convexity ≈ duration2 + dispersion (variance) of maturity. At current rates, they have the same value and the same slope (duration).

How do you calculate convexity from modified duration?

Another way to view it is, convexity is the first derivative of modified duration. By using convexity in the yield change calculation, a much closer approximation is achieved (an exact calculation would require many more terms and is not useful). Using convexity (C) and Dmod then: % Price Chg. = -1 * D mod * Yield Chg.

How do you calculate convexity?

The simplest way to calculate convexity is to use a calculator such as the bond convexity calculator at DQYDJ. You will need to know either the price or yield to maturity, how many years to maturity, face value and coupon rate.

Is convexity the derivative of duration?

Convexity is the rate that the duration changes along the yield curve. Thus, it’s the first derivative of the equation for the duration and the second derivative of the equation for the price-yield function or the function for change in bond prices following a change in interest rates.

What is convexity in math?

In mathematics, a real-valued function is called convex if the line segment between any two points on the graph of the function does not lie below the graph between the two points. Equivalently, a function is convex if its epigraph (the set of points on or above the graph of the function) is a convex set.

What is negative convexity in bonds?

Negative convexity exists when the price of a bond falls as well as interest rates, resulting in a concave yield curve. Assessing a bond’s convexity is a great way to measure and manage a portfolio’s exposure to market risk.

What is convexity of a bond portfolio?

Convexity is a risk-management tool, used to measure and manage a portfolio’s exposure to market risk. Convexity is a measure of the curvature in the relationship between bond prices and bond yields. If a bond’s duration rises and yields fall, the bond is said to have positive convexity.

What is convexity duration?

What Are Duration and Convexity? Duration measures the bond’s sensitivity to interest rate changes. Convexity relates to the interaction between a bond’s price and its yield as it experiences changes in interest rates.

What is the duration with convexity rule?

A bond’s convexity measures the sensitivity of a bond’s duration to changes in yield. Duration is an imperfect way of measuring a bond’s price change, as it indicates that this change is linear in nature when in fact it exhibits a sloped or “convex” shape.

Why is a bond convex?

So why is the relationship between a bond’s yield and its price known as convexity? As yields change, the change in the price of the bond is not linear; it is curved in a convex fashion.