What is financial accounting depreciation?

The term depreciation refers to an accounting method used to allocate the cost of a tangible or physical asset over its useful life or life expectancy. Depreciation represents how much of an asset’s value has been used.

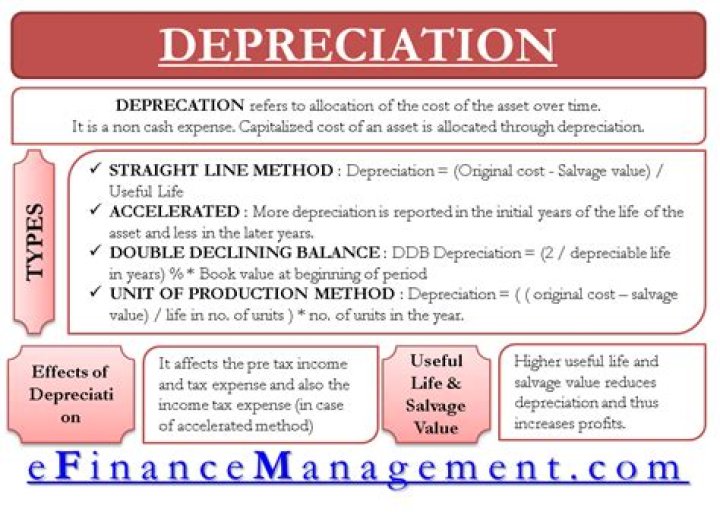

What is the formula for depreciation in accounting?

The straight-line formula used to calculate depreciation expense is: (asset’s historical cost – the asset’s estimated salvage value ) / the asset’s useful life.

How do you account for depreciation on the financial statements?

The accounting entries for depreciation are a debit to depreciation expense and a credit to fixed asset depreciation accumulation. Each recording of depreciation expense increases the depreciation cost balance and decreases the value of the asset.

What are 2 different types of depreciation?

There are four methods for depreciation: straight line, declining balance, sum-of-the-years’ digits, and units of production.

- Straight-Line Depreciation.

- Declining Balance Depreciation.

- Sum-of-the-Years’ Digits Depreciation.

- Units of Production Depreciation.

Do you include depreciation in balance sheet?

The balance sheet of a business shows the value of the assets of the business against the value of the liabilities and owner’s equity or retained earnings. Depreciation is included in the asset side of the balance sheet to show the decrease in value of capital assets at one point in time.

Where is depreciation and amortization on financial statements?

The amount of an amortization expense write-off appears in the income statement, usually within the “depreciation and amortization” line item. The accumulated amortization account appears on the balance sheet as a contra account, and is paired with and positioned after the intangible assets line item.

Which depreciation method is most common for financial reporting?

Straight-Line Method

Straight-Line Method: This is the most commonly used method for calculating depreciation. In order to calculate the value, the difference between the asset’s cost and the expected salvage value is divided by the total number of years a company expects to use it.