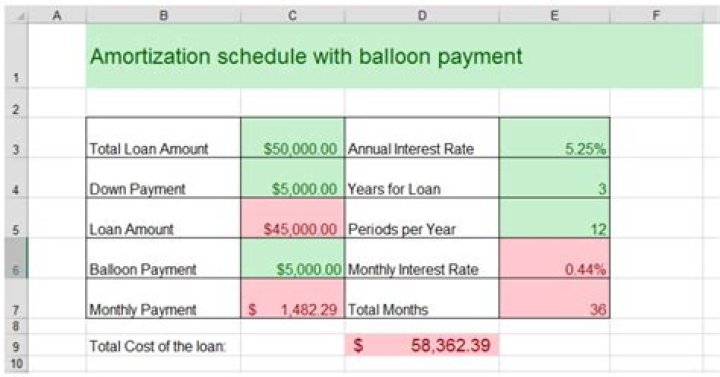

What is an amortization schedule with balloon payment?

A balloon mortgage has a short term that does not fully amortize, but the payment is usually based on a 30-year amortization schedule. Borrowers are usually required to make interest-only payments throughout the short term, after which the balloon payment is due.

Are balloon payments amortized?

A balloon loan is a type of loan that does not fully amortize over its term. Since it is not fully amortized, a balloon payment is required at the end of the term to repay the remaining principal balance of the loan.

What are 2 ways to calculate a balloon payment?

What are two ways to calculate a balloon payment? Find the present value of the payments remaining after the loan term. Amortize the loan over the loan life to find the ending balance. In the Excel setup of a loan amortization problem, which of the following occurs?

Can you pay off a balloon loan early?

Paying the balloon off early eliminates the interest the lender would have earned if you kept making the payments. The loan agreement may include penalty payments if the balloon is paid off early. Compare the penalty amounts to any interest savings you would realize from paying the loan off early.

Can you refinance a balloon payment?

You can handle a balloon payment in a variety of ways. – Refinance: When the balloon payment is due, one way to pay it off is to obtain another loan. In other words, you refinance. That loan will extend your repayment period by another 5-7 years.

How do I get rid of balloon payment?

When your balloon payment is due, you have two choices to pay it off: You can take out another mortgage for the amount of the balloon payment or you can sell your home and use the proceeds to pay it off.

What happens if you can’t pay a balloon payment?

Balloon mortgages are short-term mortgage loans that usually are due and payable within five to 10 years. If the balloon payment isn’t paid when due, the mortgage lender notifies the borrower of the default and may start foreclosure.

How are balloon payments calculated manually?

We can use the below formula to calculate the future value of the balloon payment to be made at the end of 5 years: FV = PV x (1+r)n – P x [ (1+r)n – 1 / r ] The rate of interest per annum is 8.00%, and monthly it shall be 8.00%/12, which is 0.67%.

How do you beat balloon payment?

You can handle a balloon payment in a variety of ways.

- – Refinance: When the balloon payment is due, one way to pay it off is to obtain another loan.

- – Sell the asset: Another way to deal with the repayment is to sell off the asset your purchased with the loan.

How to make an amortization schedule?

Open a new spreadsheet in Microsoft Excel.

How do I calculate an amortization schedule?

Amortized payments are calculated by dividing the principal — the balance of the amount loaned after down payment — by the number of months allotted for repayment. Next, interest is added. Interest is calculated at the current rate according to the length of the loan, usually 15, 20, or 30 years.

When should you use financing with a balloon payment?

Balance Due At Maturity. The conventional residential real estate mortgage has a structure,which includes monthly repayments of principal and interest,where the payments over the term of the loan

How is an amortization schedule calculated?

Calculations in an Amortization Schedule. The Interest portion of the payment is calculated as the rate ( r) times the previous balance, and is usually rounded to the nearest cent. The Principal portion of the payment is calculated as Amount – Interest. The new Balance is calculated by subtracting the Principal from the previous balance.