What are two disadvantages to having a defined benefit plan for retirement?

The main disadvantage of a defined benefit plan is that the employer will often require a minimum amount of service. Although private employer pension plans are backed by the Pension Benefit Guaranty Corp up to a certain amount, government pension plans don’t have the same, albeit sometimes shaky guarantees.

Do you get a tax credit for having a retirement plan?

The retirement savings contribution credit — the “saver’s credit” for short — is a tax credit worth up to $1,000 ($2,000 if married filing jointly) for mid- and low-income taxpayers who contribute to a retirement account.

Is a defined benefit plan a pension?

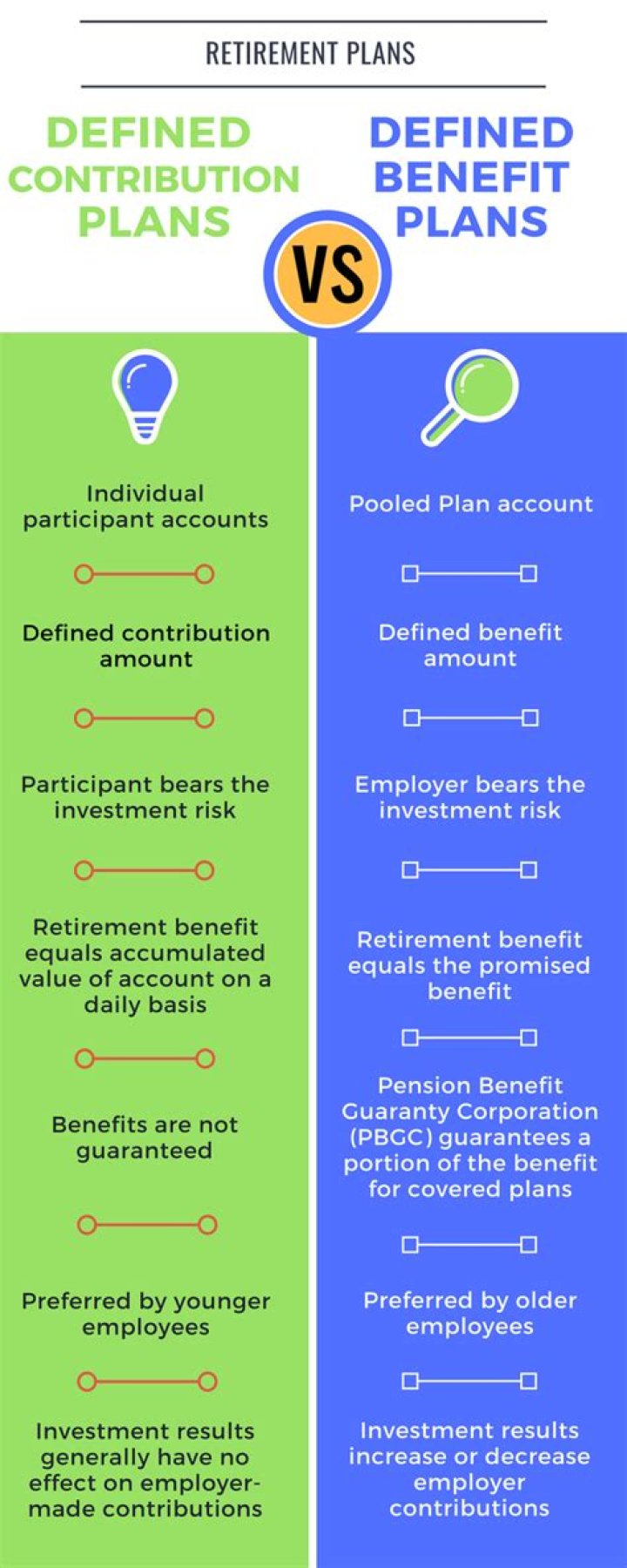

A defined-benefit plan is an employer-based program that pays benefits based on factors such as length of employment and salary history. Pensions are defined-benefit plans.

Who is not eligible to claim the saver’s credit?

This credit is not available to individuals under the age of 18, full-time students, or anyone claimed as a dependent by another taxpayer.

What are two advantages to having a defined benefit plan for retirement?

A defined benefit plan delivers retirement income with no effort on your part, other than showing up for work. And that payment lasts throughout retirement, which makes budgeting for retirement a whole lot easier.

Which is better defined benefit or defined contribution?

A Better Bang for the Buck: The Economic Efficiencies of DB Plans. This report finds that a defined benefit (DB) pension plan can deliver the same level of retirement income to a group of employees at 46% lower cost than an individual defined contribution (DC) account.

What is an example of a tax qualified retirement plan?

A qualified retirement plan is a retirement plan recognized by the IRS where investment income accumulates tax-deferred. Common examples include individual retirement accounts (IRAs), pension plans and Keogh plans. Most retirement plans offered through your job are qualified plans.

How do you get a 401k tax credit?

How can you claim this tax credit? If you qualify, you may claim the startup costs tax credit using IRS Form 8881. You can claim the credit for each of the first three years of the plan and may choose to start claiming the credit in the tax year before the tax year in which the plan becomes effective.

Is defined benefit pension income taxable?

If your spouse or partner has died and could receive pension benefits, you may receive a survivor’s pension, usually at a reduced amount. Your private pension income is fully taxable in the year(s) you receive it.

Is defined benefit pension better than defined contribution?

Defined benefit pension This is also known as a career average pension or final salary pension, and is usually a better pension type compared to a defined contribution scheme, as it guarantees a set income when you retire.

Does 401k count as retirement savings contribution credit?

You can include contributions to just about any type of retirement plan when claiming the credit, including a 401(k) plan, traditional IRA, Roth IRA, SIMPLE IRA, or 403(b) plan.

How do I get rid of retirement savings contribution credit?

Yes, you can delete the Form 8880 for the Saver’s Credit to remove it from your return. Select Tax Tools, then Tools from the navigation panel on the left. Caution: Once a form is deleted, its gone for good.