How do you record adjusting entry for depreciation?

How do you record adjusting entry for depreciation?

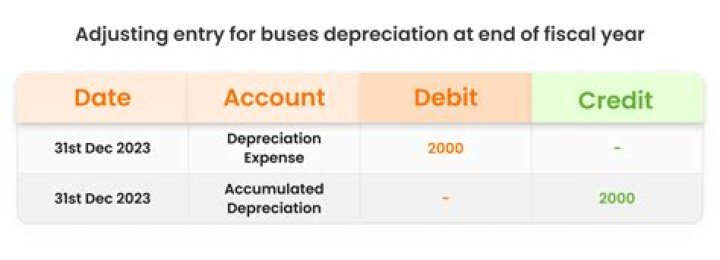

The basic journal entry for depreciation is to debit the Depreciation Expense account (which appears in the income statement) and credit the Accumulated Depreciation account (which appears in the balance sheet as a contra account that reduces the amount of fixed assets).

How do you account for a change in depreciation method?

Reporting a Change in Method of Depreciation You normally must file IRS Form 3115, Application for Change in Accounting Method, before switching the depreciation method you apply to a fixed asset. You must include a justification for your action and any supporting documents.

What are the 3 depreciation expense methods?

Your intermediate accounting textbook discusses a few different methods of depreciation. Three are based on time: straight-line, declining-balance, and sum-of-the-years’ digits. The last, units-of-production, is based on actual physical usage of the fixed asset.

What is the adjustment effect of depreciation?

Depreciation: Adjustment Entries in Final Accounts! When an asset is purchased, it does not long continue to be worth that amount. It gradually decreases in value. The asset may lose its value due to its constant use or due to its non-use (merely be passage of time).

What are adjusting entries with examples?

Here’s an example of an adjusting entry: In August, you bill a customer $5,000 for services you performed. They pay you in September. In August, you record that money in accounts receivable—as income you’re expecting to receive. Then, in September, you record the money as cash deposited in your bank account.

How do you do adjusting entries for depreciation?

The adjusting entry for a depreciation expense involves debiting depreciation expense and crediting accumulated depreciation. This is shown below. The depreciation expense appears on the income statement like any other expense.

Can you change depreciation method?

At the end of each financial year, management should review the method of depreciation. Thus, the method of depreciation can be changed without retrospective effect or with retrospective effect.

Can you switch between depreciation methods?

Taxpayers can request an automatic method change for depreciation and amortization if the requirements are met to do so. Taxpayers may change from an impermissible method of accounting to a permissible method of accounting or from one permissible method of accounting to another permissible method of accounting.

What is depreciation example?

An example of Depreciation – If a delivery truck is purchased by a company with a cost of Rs. 100,000 and the expected usage of the truck are 5 years, the business might depreciate the asset under depreciation expense as Rs. 20,000 every year for a period of 5 years.

What are the 4 methods of depreciation?

There are four methods for depreciation: straight line, declining balance, sum-of-the-years’ digits, and units of production.

How do you record adjusting depreciation?

How to Record Depreciation Expense. Depreciation is recorded by debiting Depreciation Expense and crediting Accumulated Depreciation. This is recorded at the end of the period (usually, at the end of every month, quarter, or year). Depreciation Expense: An expense account; hence, it is presented in the income statement …

How do you adjust depreciation entries?