How do you keep books of accounts in Excel?

How to Create a Bookkeeping System in Excel

- Step 1: Start with a bookkeeping Excel sheet template.

- 3 Necessary Parts of an Excel Bookkeeping System.

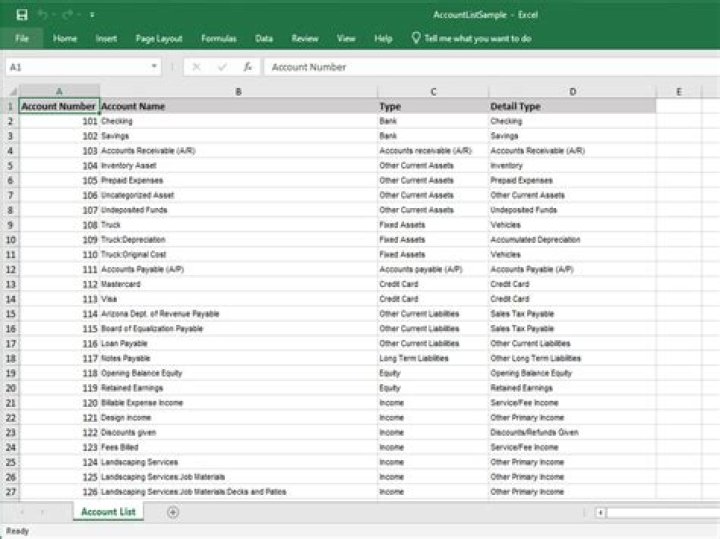

- Step 2: Customize the chart of accounts within your template.

- Step 3: Customize the income statement sheet.

- Add a sheet for tracking invoices.

Why do accountants use T accounts?

T-accounts are commonly used to prepare adjusting entries. The matching principle in accrual accounting states that all expenses must match with revenues generated during the period. The T-account guides accountants on what to enter in a ledger to get an adjusting balance so that revenues equal expenses.

What is Accounts Payable example?

Accounts payable include all of the company’s short-term debts or obligations. For example, if a restaurant owes money to a food or beverage company, those items are part of the inventory, and thus part of its trade payables.

How are T accounts used in accounting?

First, a large letter T is drawn on a page. The title of the account is then entered just above the top horizontal line, while underneath debits are listed on the left and credits are recorded on the right, separated by the vertical line of the letter T. A T-account is also called a ledger account.

How do you submit journal entries to T accounts?

Debits are always posted on the left side of the t account while credits are always posted on the right side. This means that accounts with debit balances like assets will always increase when another debit is added to the account.

How do you maintain Ledger in Excel ledger book maintain in Excel?

Open Microsoft Excel, click the “File” tab, and then choose the “New” link. When the Available Templates window appears, type “ledger” into the search box, and then click the arrow button. Excel does not have a button on the Available Templates window for its collection of ledger templates, but it does offer them.

How do you keep double entry bookkeeping in Excel?

How to Do Double-Entry Bookkeeping in Excel

- Step One: Choose Your Accounts.

- Step Two: Row 1 on Your Excel Document.

- Step Three: Formatting.

- Step Four: If-then Formulas (Columns G onward)

- Step Five: Record Your Opening Balances.

- Step Six: Record Your Expenses.

- Step Seven: Using Your Data.