Does section 382 apply to S corporations?

Does section 382 apply to S corporations?

382 applies to S corporations, and some practitioners do not agree that it does apply.

What triggers a 382 limitation?

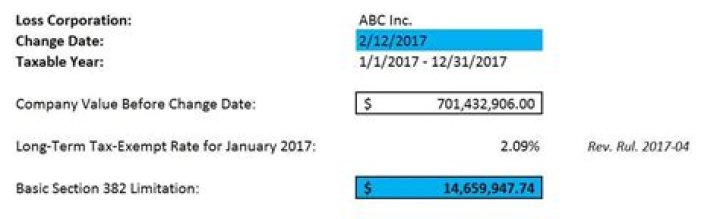

Section 382 generally limits the use of NOLs and credits following an ownership change. This occurs when one or more 5% shareholders increase their ownership, in aggregate, by more than 50% over the lowest percentage of stock owned by these shareholders at any time during the testing period, generally three years.

What are Section 382 limitations?

Sections 382 of the Tax Code limits the use of net operating losses (NOLs), and certain other tax attributes, by corporations. These provisions apply after a corporation undergoes an ownership change (i.e., a greater than 50% increase in stock ownership over, generally, a three-year period).

What are built in gains?

The built-in gains tax is a corporate-level tax on gain from certain property sales made in the recognition period following an S election by a C corporation. This gain is generally referred to as net recognized built-in gain.

What is a 383 limitation?

In general, the section 383 credit limitation is an amount equal to the tax liability of the new loss corporation for the post-change year which is attributable to so much of the corporation’s taxable income that would be reduced by allowing as a deduction its section 382 limitation remaining after accounting for the …

What is a loss corporation under 382?

Under Section 382 of the IRC, a C corporation is required to have a limit to offset historic losses. As a summary, C corporations are those under US law that are taxed separately from their owners. A loss corporation is a firm that can use tax attributes such as net operating loss (NOL) to deduct their taxable income.

What is the purpose of section 382?

Section 382 of the Internal Revenue Code generally requires a corporation to limit the amount of its income in future years that can be offset by historic losses, i.e., net operating loss (NOL) carryforwards and certain built-in losses, after a corporation has undergone an ownership change.

Can an S Corp have capital gains?

Because the S-corp is a “pass-through” business, it pays no capital gains taxes on the sale.

How many years is an S corporation subject to built in gains tax?

five-year

Overview of built-in gains tax The built-in gains (BIG) tax generally applies to C corporations that make an S corporation election, and it can be assessed during the five-year period beginning with the first day of the first tax year for which the S election is effective.

What is SRLY limitation?

The SRLY rules are designed to limit the extent to which a consolidated group can claim a CNOL deduction that is attributable to NOLs generated in years in which the attributable member was not a member of the group.